Broken Promises

22. Jan 2016

Cost of coal and copper production carried by people and the environment

1

The African continent has abundant natural resources and is a major exporter of valuable raw materials. For half a century, the riches underground have brought foreign companies to the region in their quest to find new ways to feed the world’s growing demand for fuel, metals and minerals. This investigation, ‘Broken Promises’, looks into both the short-term effects of extractive industry in Mozambique, and its long-term effects in Zambia, where mining has been going on for almost a century.

During the past two decades, thousands of people in Mozambique and Zambia have sacrificed their health and livelihoods to make way for fast-growing mining industries. In the case of Mozambique, mining companies have knowingly resettled communities to areas with restricted access to food, water and transportation, posing an immediate challenge to their livelihoods.

In Zambia, public health and the environment have been severely affected in many ways, some irreversible, by pollution from mining. This investigation finds that revenues from the billion-dollar mining industry have left Zambia through illicit cash flows, and have therefore not resulted in the country’s development, which is a violation of their basic

human rights.

Displacement of thousands

The ‘Broken Promises’ investigation shows that at least three of the biggest steel companies in Europe are sourcing coking coal from mines in Mozambique, where people and communities have been removed and resettled with insufficient compensation and housing, and unreliable access to water and jobs.

In 2009-2010, the government of Mozambique and international mining companies initiated two major resettlements. One of the world’s largest mining companies, Brazil’s Vale, moved thousands of people to the Cateme resettlement. In subsequent years, in Moatize, 736 families were removed from their homes at the Revuboè riverside by Riversdale (Australian), Rio Tinto (British-Australian), Tata Steel (British-Indian)

and ICVL (Indian).

In June 2015, Danwatch interviewed a large number of community members in the Cateme and Mualadzi resettlements in the Tete province of central Mozambique. The communities tell similar stories of never receiving the compensation they were promised and to which they are legally entitled. They describe major deterioration in living standards as well as livelihoods threatened by the lack of water, food and jobs in the new

resettlement.

According to national mining law and international guidelines, resettlements are not permitted unless people are compensated fairly and are able to maintain their livelihoods. It is the duty of Mozambique to protect human rights, and the duty of companies to respect them, according to the UN’s Guiding Principles on Business and Human Rights. These include the right to food, water and adequate housing, as defined in Article 25 of the Universal Declaration of Human Rights (UDHR) and Article 11 of the International Covenant on Economic, Social and Cultural Rights.

Nevertheless, the government and mining companies moved communities to Mualadzi, knowing full well the location lacked sufficient access to water, according to the Resettlement Action Plan obtained by Danwatch. According to the UN human rights conventions to which Mozambique is a signatory, companies with activities in Mozambique are obliged to make sure that: “Operations do not adversely impact local or regional access to adequate food or the availability, accessibility and quality of clean water in both the short and long term.”

None of the steel companies that source from Mozambique has been willing to comment directly on the findings in this investigation.

Browse the photos and read the stories about the people of Mualadzi.

The resource curse in Zambia

In neighbouring Zambia, where foreign direct investments (FDI) in the Copperbelt region began more than 50 years ago, the consequences have been dire. Air and water pollution have been some of the direct impacts of copper mining, affecting people’s lives and the environment.

Zambia is the second-largest producer of copper in Africa, and according to the US Geological Survey 2015, the eighth largest in the world. But the attentions of foreign investors and comprehensive extractive mega-projects have had little effect on the share of people living below the poverty line. Tax abuse is one reason. Tax avoidance or manipulation by multinational mining companies is draining the country of billions of dollars in resources meant for development. On the other hand, systematic tax abuse is only possible because of a lack of regulation and enforcement, which means that the state is again failing to protect its people’s human rights. Tax abuse, poverty and violation of human rights are deeply entwined, because tax abuses deprive governments of the resources required to ensure the economic, social and cultural rights, according to the report “Tax Abuses, Poverty and Human Rights” (2013) issued by the International Bar Association’s Human Rights Institute (IBAHRI).

In parts of the country, the long-term effects of copper mining have resulted in pollution of local waterways and have caused catastrophic damage to people’s health and livelihoods. While extractive industries are a significant source of economic growth for resource-rich countries, their serious downsides have frequently been called the ’resource curse’.

How copper is sneaking off the books

2

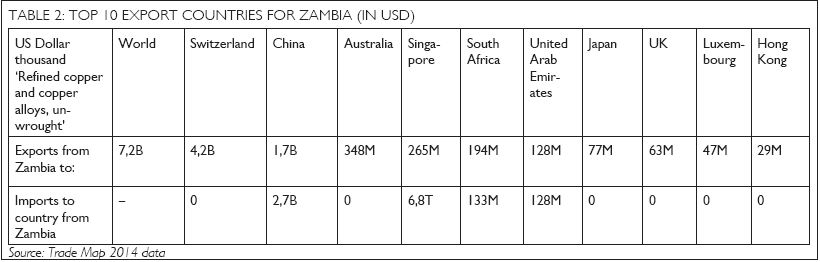

In 2014, copper worth billions of dollars seems to have disappeared on its way from Zambia to Switzerland. A first glance at trade statistics from Trade Map shows that ‘copper and articles thereof’ valued at USD 4.2 billion were exported to Zambia’s largest export market for copper, Switzerland. But the same database shows that Switzerland did not import any ‘copper and articles thereof’ at all from Zambia in 2014.

What happened to the copper?

It never went to Switzerland, says Dr. Andreas Missbach, head of the Commodities, Trade and Finance Department, Berne Declaration. “Switzerland appears in Zambian statistics of copper exports because a multinational Swiss-based company exports a lot of that copper. But it is not going physically to Switzerland. The business model of commodity traders is called ‘transit trade’, since the products never reach Switzerland. They are going directly to end users everywhere.”

This is confirmed by Nkula Edward Goma, a former programme officer at Center for Trade Policy in Zambia and from one of the CSO’s, who raised the case against Glencore. This article looks into the various trade and tax schemes that multinational mining companies use in order to lower their tax rates and increase their profits from extracting resources in Zambia; these practices have demonstrated long-term impacts, including illicit cash flows out of the country at the expense of the Zambian people and of their basic human rights.

Transfer mispricing is draining Zambia

Discrepancies in trade data show up for many reasons – countries may use different valuation methods or different types of trade recording systems – but the fact that the discrepancies are so large that Switzerland’s import of copper from Zambia does not even appear in trade statistics is an indicator that transfer mispricing is going on, said two researchers, Mwanda Phiri and Shebo Nalishebo from the Zambia Institute for Policy Analysis and Research, in the Zambia Daily Mail, March 2015.

Transfer pricing happens whenever two companies from the same multinational group trade with each other, establishing a price for the transaction; this is not illegal. Transfer mis-pricing, or re-invoicing, happens when goods leave the exporting country under one invoice, and the invoice is re-directed to the purchaser’s subsidiary in another country (usually a tax haven), where the price is altered. The revised invoice is then sent to the purchaser in the importing country for payment. This allows a multinational company to shift profits to subsidiaries located in countries with lower tax rates, thereby increasing the company’s overall profits; this practice is considered abusive and illegal.

WORLD RESOURCES OF COPPER

A 2014 USGS global assessment of copper deposits indicated that known World resources of copper contain about 2.1 billion tons and undiscovered resources contain an estimated 3.5 billion tons.

Source: US Geological Survey 2015

Transfer mispricing accounted for 80 percent of illicit financial flows out of developing countries over the last decade, which translates to an estimated USD 4.688 trillion of estimated USD 5.86 trillion in total illicit financial flows, according to IBAHRI. The phenomenon appears to be widespread, since the majority of global trade happens across borders, but within multinational companies. One example comes from a report leaked from auditing firm Grant Thornton in 2012 that found evidence that Glencore International was transferring profits to Switzerland, where the company would pay a lower tax rate, in violation of OECD guidelines.

According to the NGO Action Aid, the company’s tax practises cost the Zambian government as much as £76 million per year in lost corporate taxes. Grant Thornton never confirmed the report, and the case against Glencore was settled with OECD’s National Contact Point in Switzerland. Glencore said all transactions were conducted on an arm’s-length basis and at internationally agreed prices. Eventually, the case was dismissed. Transfer pricing is among the greatest tax abuses in developing countries,

according to IBAHRI. Other abuses include the negotiation of tax holidays and incentives; the taxation of natural resources; and the use of offshore investment accounts.

“Secrecy jurisdictions are also a concern because of their role in facilitating tax abuses. International standards that promote greater transparency and more effective exchange of information for tax purposes need to be further developed,” the IBAHRI report states.

Poverty prevails

Zambia is the second-biggest producer of copper in Africa, and the seventh largest in the world, according to World Copper Factbook; it is the eighth largest according to the US Geological Survey 2014. This landlocked country in the southern part of Africa has abundant natural resources, including cobalt, zinc, uranium and gemstones, yet it remains one of the poorest countries in the world.

Copper is Zambia’s leading industry. It accounts for more than 70 percent of Zambia’s export earnings and 12 percent of government revenue. Zambia produced more than 700,000 metric tons of copper in 2014, and is on track to do so again in 2015, said the Minister of Mines, Energy and Water Development in Zambia, Christopher Yaluma, to Bloomberg in June. Despite Zambia’s valuable resources, according to the World Bank, 60 percent of Zambians live in poverty and 42 percent in extreme poverty, living on less than USD 1.25 per day. Transfer mispricing is the main reason for this. Between 1970 and 2010, illicit cash flows due to transfer mispricing amounted to an estimated a loss to the country of USD 17.3 billion (in 2010 prices), according to a 2013 UN paper on Zambian mineral extraction, “Capturing Mineral Revenues in Zambia.”

Tax abuse hinders human rights

Tax abuse has considerable negative impacts on human rights, because it deprives governments of the resources required both to offer programmes that support economic, social and cultural rights, and to create and strengthen the institutions that uphold civil and political rights, suggests the International Bar Association’s Human Rights Institute (IBAHRI). Simply put, tax abuse hinders development and is therefore a violation of several human rights. The UN Special Rapporteur on Extreme Poverty and Human Rights has illustrated how poverty is connected, whether as cause or consequence, to violations of fourteen different human rights, including the rights to food, to health, to education, to social security, and to the principle of transparency.

COPPER

Copper is a metal that has been used by humans for over 10,000 years. Today copper and its alloys are indispensable in the electronics industry due to their excellent conductive properties, as copper is mainly used in wires, cables and other electrical equipment. Zambia holds six percent of the world’s known copper reserves, though the World Bank estimates that its real share could be greater.

Source: World Bank and World Copper Factbook 2014

In Zambia, this is indeed the case. The country is far from reaching the UN’s Millennium Development Goals, which include reducing poverty and maternal mortality, preventing new HIV infections, and ensuring that children complete secondary school. These are all indicators that progress and human development are happening way too slowly in a country with enormous underground resources.

Who is responsible?

The Zambian state has the responsibility to protect its citizens’ human rights, and the mining companies have the responsibility to respect human rights, according to the UN Guiding Principles on Business and Human Rights.

COPPER MINE PRODUCTION IN ZAMBIA

Zambia is the 13th largest producer of copper in the world

2013: 760 tons

2014: 730 tons

reserves: 20,000

World total (rounded)

2013: 18,300 tons

2014: 18,700 tons

Reserves: 700,000

Source: USGS 2015

To begin with the latter, companies must have appropriate policies and due diligence procedures in place to ensure that their activities do not have negative impacts on human rights. This means that multinational enterprises, as well as their advisers and financiers, should acknowledge and act to redress the ways that their tax planning strategies can negatively impact human rights. Since the negative impacts that tax abuse has on poverty and human rights are so severe, the state has a number of obligations to counter tax abuse, according to the IBAHRI report “Tax Abuses, Poverty and Human Rights” (2013), which states:

“These flow from the state’s obligation to use the maximum available resources to progressively realise human rights including the obligation to confront tax abuses as part of an overall plan to strengthen financial and tax governance. Furthermore, states have the obligation to ensure coherence between corporate, fiscal, tax and human rights laws and policies, both at the domestic and international levels.

MARKET SHARE OF THE FIVE LARGEST COPPER PRODUCERS

Kansanshi mining, owned by First Quantum Minerals: 35 percent

Konkola copper mines, owned by Vedanta Resources: 17 percent

Lumwana mining company, owned by Barrick Gold: 15 percent

Mopani Copper mines, owned by Glencore: 15 percent

CNMC Luanshya Copper mines, owned by China Nonferrous Metal Mining: 5 percent

Source: EITI, 2013

This includes the corollary obligations to avoid corporate, fiscal or tax measures that have retrogressive impacts on human rights. The obligation to do no harm with respect to economic, social and cultural rights should be understood to include an obligation for states to assess and address the domestic and international impacts of corporate, fiscal and tax policies on human rights.”

Indeed, the UN’s Guiding Principles on Business and Human Rights imply access to remedy provided by the state. The ‘Access to Remedy’ principles focus on ensuring that where people are harmed by business activities, there is both adequate accountability and effective redress, both judicial and non-judicial.

In the case of the Zambian state, this translates into not only strengthening fiscal and tax governance and enforcement capacity, but also ensuring transparency and access to information. Danwatch has tried to contact the Zambian Revenue Authority for comment by email, but there has been no response.

Impacts of copper mining on people and nature

3

Although few in number, the multinational mining companies that are earning billion-dollar profits in Zambia have had a massive impact on its environment and people. On the bright side, the copper mining industry records the country’s largest export earnings and has generated more than 90,000 jobs for Zambians today.

For almost 100 years, Zambia has been highly dependent on copper and the mining industry, and the country is living proof that progress leaves its mark on both the environment and people’s health. Land degradation. Increased deforestation. Water and air pollution from particles of sulphuric acid, which severely affect those residing near mines. These are some of the main concerns of The Environmental Council of Zambia.

‘People can’t live here’

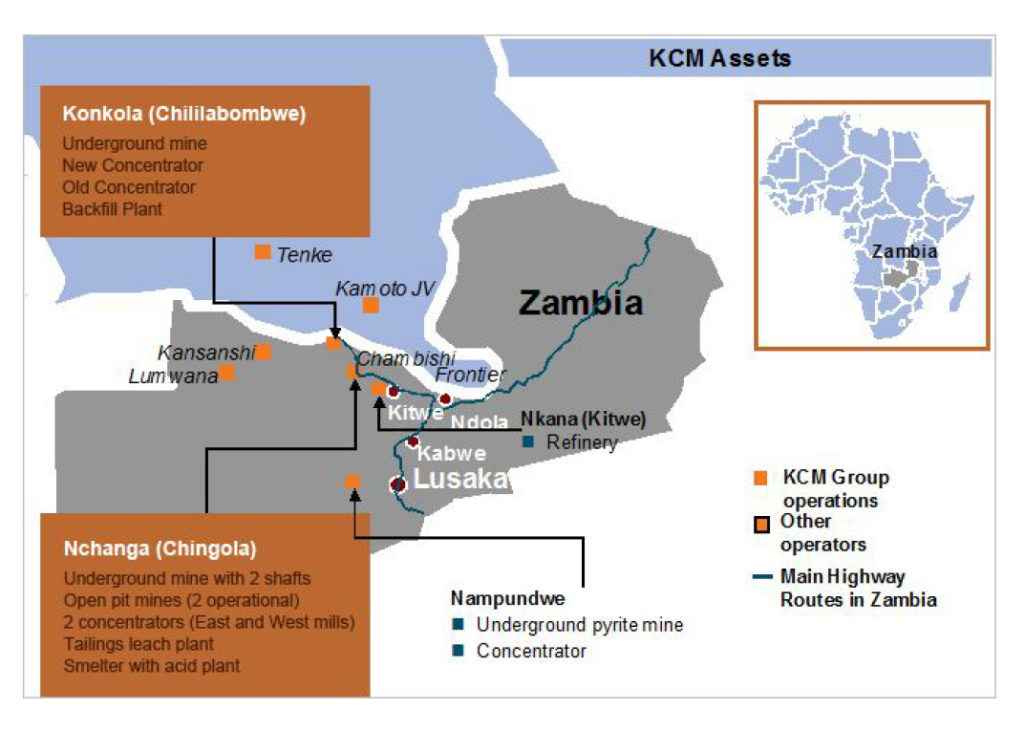

In August 2015, 1,800 local residents from Shimulala and nearby villages in Zambia sued the mining giant Vedanta Resources and their subsidiary KCM, claiming that copper extraction from the Konkola mine – the largest copper mine in Africa – is polluting the local waterways and causing catastrophic damage to their health and livelihoods.

According to a leaked confidential internal report commissioned from Canadian pollution control experts, Vedanta Resources’ giant mine in Zambia’s Copperbelt region has been spilling sulphuric acid and other toxic chemicals into the rivers, streams and underground aquifers used for drinking water near the mining town of Chingola.

“It is not possible to live in this area any longer,” said one resident, Leo Moulenga, in an interview with The Guardian in August 2015.

“The ground is contaminated, our crop yield has dropped. In the future we don’t think people will be able to live here. It is becoming uninhabitable.”

According to the Blacksmith Institute, an American environmental research centre that monitors Chingola province, 93,000 tons of industrial waste are produced in the area every year, most of which is dumped in the Kafue River. The Blacksmith Institute’s investigations have concluded that the primary polluter is the Konkola copper mine, and the consequences are dire: The pollution constitutes a direct and imminent health risk for both human and animal life, and could lead to outbreaks of cholera if not halted. Allegations of environmental and human rights violations are not unusual in the Zambian

mining industry.

Health risk for humans

In 2008, a malfunctioning pump at the Mopani mine led to acidic residue polluting the nearby water network that services the surrounding communities with drinking water. Local clinics registered over 1,000 residents affected by the spill, who complained of abdominal pains, diarrhoea and vomiting. While the owners, mining companies Glencore and First Quantum, maintained that this was a tragic accident, critics claimed that the companies were neglecting their environmental responsibility.

The government legally charged and fined a mine manager and three other employees at Mopani Copper Mines for the pollution of the Mufulira water system, saying the company polluted the water supply system for 800 residents in the small mining city of Mufulira. At that time, mines and mineral development minister Kalombo Mwansa began reviewing legislation to attach stiffer penalties to violations by companies and officials, according to Business and Human Rights.

It’s in the air and water

The mining industry uses sulphuric acid in the extraction and treatment of copper. The extraction processes are called heap and situ leaching; during these processes, particles react with each other to create acidic mists that not only harm people’s skin, eyes and lungs, but also destroy crops, deteriorate the quality of the land, and damage nearby buildings. The acid dust both smells and tastes bad.

“We took a sample of the water, which was cloudy and had a foul smell. A few minutes later the colour of the water turned bright orange, and the smell was overpowering,” a BBC journalist, Nomsa Maseko, recently reported from Hippo Pool village by the Kafue River. Several epidemiological studies have suggested a correlation between exposure to inorganic acid mists containing sulphuric acid and an increased incidence of laryngeal cancer. The International Agency for Research on Cancer (IARC) has concluded that ”occupational exposure to strong inorganic mists containing sulphuric acid is carcinogenic for humans.”

Nevertheless, sulphuric acid is still used with little concern for the people affected through air and water pollution, and the environment and animal life continue to be severely affected by copper extraction in Zambia.

Long way round: How Zambian copper is entering the EU

4

Copper enters the global market in many shapes and sizes: copper concentrates, blister and anode, cathode and ingots, scrap, semis and powders, and compounds. All forms are traded globally. Copper is traded along every link in the supply chain, from the mine to the end-user product. It must first be smelted, refined and transformed into shapes or alloys before it is ready for fabrication in brass mills, foundries, wire mills or other plants. In the final stage, industries transform the copper into end-use products such as cars, domestic appliances, electronic equipment, etc.

The supply chain for copper is complex due to the high level of copper recycling, which cannot be distinguished from primary copper once it is reprocessed. This involves different trade schemes in which the copper is sold many times through many countries before it is shipped directly to the end-user country. This article attempts to map the global supply chain for copper, with a specific focus on European end-users. What is the link between Zambia’s copper mining industry and European consumers?

From the mines in Zambia

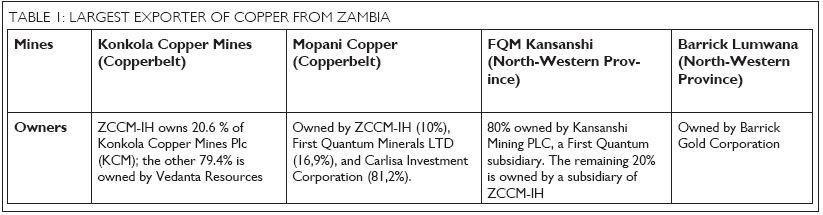

Four companies account for more than 70 percent of Zambia’s copper production, according to a survey by the International Council on Mining and Metals. These mine owners are Vedanta Resources, Barrick Gold Corporation, First Quantum Minerals (FQM) and Carlisa Investment Corporation, the latter a joint venture between Glencore and FQM.

The last two companies rank third and tenth respectively in Thomson Reuters GFMS’ Copper Survey Top Ten from June 2015. The table shows the ownership structure of the four Zambian mines. ZCCM-IH refers to Zambia Consolidated Copper Mines Investment Holdings Plc., whose majority shareholder is the government of Zambia. See table 1.

Export of copper from Zambia

Zambia exported copper valued at approximately USD 7,2 billion in 2014. Its main importer of refined copper was Switzerland, while the main destination for its unrefined copper – 95 percent of the total – was China, according to The Atlas of Economic Complexity. Zambia’s 10 biggest export countries for ‘refined copper and copper alloys’ ‘can be seen below. See table 2.

Re-export of copper from Switzerland

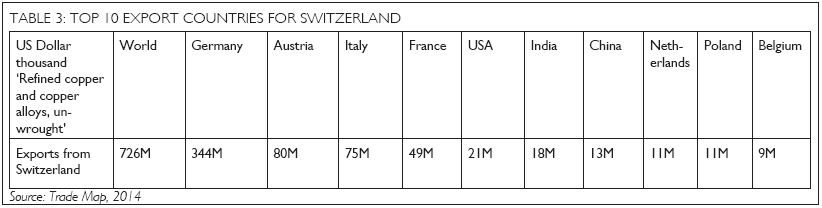

The discrepancy between exports from Zambia to Switzerland and imports to Switzerland from Zambia suggests that the copper never reaches Switzerland, but is instead bought and sold by Swiss-based traders and exported directly to manufacturers, who use copper in the production of electrical equipment or wire or construction of buildings. See table 3.

Global consumption of copper in end-user products

Copper are in products that are used every day. The industries reliant on copper for the production of end-user products is divided into five categories: building construction, electrical & electronic products, transportation equipment, consumer & general products, and industrial machinery & equipment. According to the World Copper Factbook, the latter is the largest copper-consuming industry, with a share of 31 percent in 2013; however, the Thomson Reuters Survey, electronics and electrical equipment is by far the largest copper-consuming industry with a global share of 39 percent. The discrepancy may be due to different ways of categorizing, but the overall picture remains. Electrical equipment and building construction are the industries with highest demands for copper.

China is the leading global consumer of copper, accounting for 44 percent of world demand in 2014. China’s demand for copper in electronics and electrical equipment is not primarily related to IT manufacturing, which requires fairly small amounts of copper, but instead to the country’s shift from coal power to electricity. This has required a rapid expansion of electrical grids. Furthermore, the expansion of the green energy sector has increased demands for wind turbines and photovoltaic panels, which are copper-intensive. Some wind farms contain over 91,000 metres of copper wire, according to The Copper Alliance.

40 to 50 percent of annual EU copper demand is sourced through recycling, which makes the supply chain even less transparent. The EU accounted for 15-19 percent of the global end-use of copper in 2014, which means copper for end use with manufacturers that makes products for consumers.

The International Copper Study Group indicates that the EU’s apparent annual refined copper usage was 3.2 million metric tons in 2014, an increase of 6 percent from the year before. 38 percent of the EU’s share of copper, or around 1,210,000 metric tons, was used in the building construction industry, making it the biggest end-user industry in EU.

INTERNATIONAL COPPER ALLIANCE - LEADING COPPER PRODUCERS IN THE WORLD

International Copper Alliance’s 43 members represent a majority of the world’s primary copper producers, some of the largest mid-stream smelter/ refiners, and 11 of the world’s largest copper fabricators.

COPPER IN THE WORLD

According to the United States Geological Survey (USGS), copper reserves amount to 690 million tons (Mt) and identified and undiscovered copper resources are currently estimated to be around 2.1 billion tons and 3.5 billion tons, respectively (basis 2013). The latter does not take into account the vast amounts of copper found in deep sea nodules and land‐based and submarine massive sulphides.

Source: International Copper Study Group

ICA MEMBERS

Anglo American

Antofagasta Minerals S.A.

Aurubis

BHP Billiton Plc

Boliden AB

Buenavista del Cobre, S.A. de C.V.

Chinalco Luoyang

Compañia Minera Doña Inez Collahuasi

Compañía Minera Zaldívar

CODELCO-Chile

Daechang Co., Ltd.

Freeport McMoRan Inc.

Glencore

Golden Dragon Precise Copper Tube

Halcor S.A.

Kennecott Utah Copper Corp.

KGHM Polska Miedź S.A.

KME

LS-Nikko Copper Inc.

Luvata

Méxicana de Cobre, S.A. de C.V.

Minera Alumbrera Ltd.

Minera Antamina S.A.

Minera Centinela

Minera Escondida Limitada

Minera Los Pelambres

Mitsubishi Materials Corporation

Mueller Industries

Nexans

Outotec Oyj

Palabora

Pan Pacific Copper

Revere Copper Products, Inc.

Rio Tinto Plc

Sociedad Contractual Minera el Abra

Sociedad Minera Cerro Verde S.A.A.

Southern Copper Corporation

Sumitomo Metal Mining Co., Ltd.

Teck

Tenke Fungurume

Wieland-Werke AG

Yunnan Copper Industry (Group) Co., Ltd.

Poverty in Mozambique: Fast growth is not the answer

5

The steady rise of the skyline over Maputo, the capital of Mozambique, has not yet slowed. Economic growth in one of the world’s poorest countries has accelerated over the last 20 years to more than seven percent annually and today Mozambique is one of the fastest-growing economies in Africa. According to the African Development Bank, the main drivers of growth are FDI and a boom in the extractive industries, propelled by a

boost in coal exports.

The growing economy is good news for the people who live in the central urban areas of Mozambique, but less so for the poor majority who live in the rural areas. The massive growth has not been accompanied by a decline in the country’s poverty rate, which in 2013 caused UN special rapporteur on human rights and extreme poverty, Magdalena Sepulveda, to raise concerns. She pointed out that Mozambique was about to miss a historic opportunity to use the newfound wealth to alleviate poverty and better the lives for the poorest part of the population.

“There is a risk that those living in poverty in Mozambique will be left behind as the country enters a period of unprecedented economic growth with extractive industries vying to invest in the country’s rich natural resources,” she said, calling on the government to urgently respond to the needs of the poorest and most marginalised in society.

An economic fairy tale in Africa

The impressive growth story began with a joint venture in 1998 between the government of Mozambique and BHP Billiton and Mitsubishi Corp in relation to the USD 2.4 billion Mozal Aluminium Smelter Project. The Mozal project was the first major FDI project in Mozambique since the end of the country’s devastating civil war in 1992 and it promised to triple the country’s exports and push growth to previously unseen heights. According to the World Bank, exports from the Mozal Smelter added more than seven percent to the country’s GDP in its initial years.

After the civil war that ravaged the country for two decades, Mozambique adopted an economic development strategy that embraced foreign investment in large-scale mining projects. This marked a new era where a massive boom in FDI contributed in a steep rise to the country’s growth rate. Since 2007, multi-billion dollar investments have been made into mega coal mines and large-scale transport infrastructure.

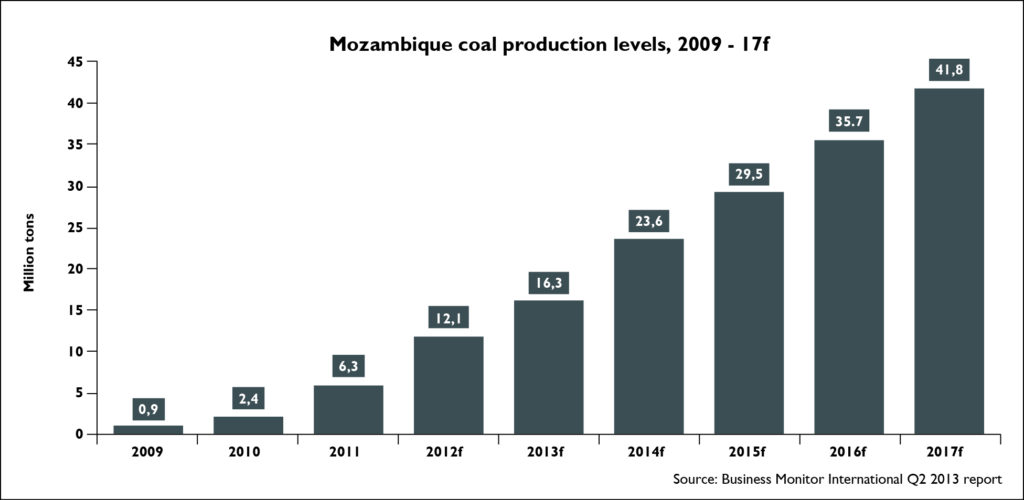

Mozambique’s subterranean wealth is still attracting a steady flow of foreign investors and mining corporations to the country. Over an eight-year period, FDI grew explosively from approximately USD 122 million in 2005 to over USD 6 billion in 2013, according to World Bank. The size of the extractive sector in Mozambique grew by 22 percent in 2013, largely because of the surge in coal production which, according to African Economic Outlook, increased from 4.8 million ton in 2012 to 7.5 tons in 2013.

Today the map of Mozambique is marked with a vast number of concessions and licences sold to foreign investors. Once a deserted area, the Tete province in central Mozambique has turned into a lucrative centre for extractive industries. As Ben James, managing director of Australian mining house Baobab Resources, recently said to the International Resource Journal:

“By 2025 Tete could be producing 25 percent of the world’s coking coal.”

The ground under Tete is rich with coking coal, which is used worldwide as a vital part of traditional crude steel production. In 2013 African Outlook named the extractive sector one of the fastest growing in Mozambique, largely led by a boost in coal exports. The same year, Mozambique was among the global top ten coking coal exporters with 4 million tons exported, according to numbers from the World Steel Association. The country’s export of coke and semi-coke to the EU market alone was 630,487 tons, according to the ITC Trade Map – a remarkable number given that in previous years there is no registered export to Europe.

The extractive industries is a growing business, according to the latest report from the Extractive Industries Transparency Initiative on Mozambique (2012), which is based on the government’s own numbers:

“Extractive industries contributed 2 percent of GDP in 2012. However, investment in the mining and hydrocarbon sectors is growing significantly, promising a rapid expansion of the sectors in the next few years. The oil, gas and mining industry was the fastest growing sector in 2012 and helped propel GDP growth to 7.4 percent. Payments from oil and gas

companies represented 80 percent of the government’s extractive revenue in 2012, while mining companies contributed 20 percent.”

Poverty still prevails

In order for the benefits of a growing resource sector to reach society in general and the poorest people specifically, the extractive industries will have to “contribute to sustainable and broad-based growth,” the World Bank states in its country profile of Mozambique.

“Recent mega-projects in coal, mineral-sands and natural-gas extraction and processing have thus far had only a limited impact on employment and poverty reduction. Some of the challenges ahead include the formulation of strategies for developing Mozambique’s coal and natural gas reserves, determining how these industries interact with other economic sectors, and ensuring that the expected increase in natural resource revenues are used in the most effective way, avoiding the fate of many other natural resource rich countries.”

Despite growth, poverty still prevails, and in some areas it has got even worse. Even though Mozambique has experienced a rise in life expectancy and expected years of schooling, the average Mozambican can expect to live for only 59.4 years, and the quality of education remains too low, according to the UN Human Development Report 2014.

Mozambique is still among the 10 poorest countries in the world, ranking as number 178 out of 187 countries and territories on the UN Human Development Index (HDI). More than half of the population (55 percent) live below the national poverty line and the largest part of the poor population live in rural areas, where they depend on subsistence farming, according to African Economic Outlook 2015. The country’s elite has to secure a more even distribution of the country’s newfound wealth, said UN special rapporteur Magdalena Sepulveda in April 2013.

“It is an unavoidable fact that significant numbers of Mozambicans are living in extreme deprivation and social exclusion. Therefore, those better off in society should strengthen their efforts to ensure everyone can lead a dignified life, a goal that is certainly achievable even within the limited resources of the country.”

In the June 2014 country report presented for the Human Rights Council, the recommendations from the UN special rapporteur to the government of Mozambique were clear:

“As Mozambique enters a period of economic growth, there is a real and tangible opportunity to eradicate extreme poverty, with great potential for future shared prosperity for everyone. The effective implementation of poverty reduction strategies must be considered a matter of priority.”

Where does the money go?

Political and military tensions in Mozambique escalated in 2014 with violent confrontations between the Renamo opposition and government forces, resulting in civilian deaths, displacement of people and overall disruption of all socio-economic activities. The situation stabilised in September 2014 when the parties signed a peace agreement. The power structure in Mozambique does not allow for any significant change in the country’s distribution policies, says associate professor Lars Buur from Roskilde University and author of The Politics of African Industrial Policy (2015).

“The top leadership, those in charge of the Frelimo Party, make sure that the revenues will continue to benefit the ruling elite.”

According to Lars Buur who has done extensive research into Mozambique’s economic and political landscape, the Frelimo party state has up to 4 million members but is governed by an old post-independence top leadership group of 50 families, among whom 10 families hold the actual power.

“They make sure that all contracts benefit people inside their circle of trust,” he explains.

A high level of corruption and low level of accountability are barriers to development. Mozambique has a score of 30 on the Transparency International’s Corruption Perceptions Index (CPI), where most corrupt country scores 0 and the least corrupt 100. According to an analysis from Transparency International (2014), patronage and favouritism is a common practice in Mozambique.

“The fact that the executive government concentrates much of the power and is responsible for the appointment of public officials in different government agencies and bodies, makes the reliance on personal and partisan relationships more prominent.”

Distribution is the key

Favouritism and patronage is not necessarily a problem in itself when it comes to economic growth. The question is how the wealth is distributed, says Lars Buur.

“In Mozambique, distribution is where the real problem lies. In order to control accumulation, the government and the ruling elite will work against economic activities that could actually be very beneficial for the country as a whole because they fear the money could then fall into the hands of opposition. That kind of patronage, corruption or favouritism is very detrimental to economic growth.”

Despite recent efforts to strengthen the country’s tax system by replacing the previous regime with a new mining tax law largely developed by international consultants and experts from the donor community, the reform is unlikely to lead to a more even distribution of wealth in Mozambique, says Buur.

“Despite some weaknesses, the tax laws are of a far better quality than many of the laws we know from Europe. The big issue is how you implement it – to what extent you set up the institutions and give political space for them to work. That is the real battleground,” he says, stressing that laws are worth little without the political will to implement and enforce them.

Displaced from the Riverside to Barren Land

6

“People are struggling. Where we used to live, we had many things to do, we used to farm, sell bricks, charcoal and firewood, but here there is no market for it. If you look around you will see houses without roofing, because people have sold it to get some money,” Domingo Foguete from the mining province Tete in Mozambique, explains. For a year he has been wrangling with the government and the mining company Vale to get compensation for the land he lost when his family first moved to Cateme.

“That was in 2010 and we still haven’t received any money,” he says. He belongs to one of the hundreds of families in the Tete province that have been were moved away when mining companies moved in. Both national law and international guidelines clearly state that the living standards of the resettlement should be at least at the level of the previous residence, but ”this Danwatch investigation finds not only that the resettlements

are far from satisfactory, but that the mining companies knew of this before

they moved the families.”

During 2009-2010, 716 families classified by Vale as “rural” were moved to the locality of Cateme, about 40 kilometres from their homes near the district capital Moatize, while 288 families regarded as “semi-urban” were resettled inside Moatize. In accordance with Mozambique national law, the families were compensated, but today the people in Cateme point to major shortcomings in the resettlement. Vale failed to deliver on their promises and the government failed in keeping the company accountable, they say.

In the course of their first years in Cateme, the resettled families had to live without access to farmland and without a reliable water supply. According to a 2013 Human Rights Watch report, ‘What is a House Without Food?’, the government’s allocation of land was delayed for three years and most repairs to a deficient water system did not take place until 2012- 2013, four years after the resettlement was initiated.

Cracked houses and leaking roofs

At a first glance the pastel-painted houses provided by Vale look as if they were build to last, but a closer look reveals that they have been placed directly on the ground. Built with no foundation, they will float away like tiny Monopoly pieces when the rainy season turns the red dusty ground into mud.

On the 1st of February 2011, Albertina Tivane, head of the Provincial Resettlement Commission admitted to “some problems in the house building process,” and added that some had “likely not been corrected,” the online news media Deutsche Welle wrote. Today, the houses are still deteriorating with visible cracks in the walls.

“The only thing separating the houses from the ground is a sheet of plastic, so the houses are cracking,” says Delvino Xadreque, a young farmer, pointing to a long line running upward from the corner of his house. He and his household of eight were lucky, because they had the means to build an additional house next to the two-room cottage provided by the company.

Years after Vale started its mining activities in Chipanga, the conflict still hasn’t been solved. Danwatch has tried to interview both the mining company, Vale, and the Ministry of Natural Resources in Mozambique about the process around the resettlement and the current situation in Cateme, but both declined to answer. Vale has also declined to share any documents from the Resettlement Action Plan for Cateme. In an email to Danwatch, Vale states that they decline to participate in an interview because the company has adopted a “low profile strategy” on Mozambique.

A cause for concern

The case of Cateme is one of many examples of people being removed from their land and homes when corporations move in to search for coal, gas and minerals in Mozambique. Since the peace accord in 1992, the country has opened its doors to a growing number of international corporations while securing a massive influx of foreign investment. A list from the Ministry of Mineral Resources, obtained by the Center for Public Integrity Mozambique, shows that by 2012, the government had issued more than 700 licences and concessions, causing thousands to leave their homes.

Rich in coal, the Tete province in central Mozambique is now the epicentre of the country’s mining industry and its land is largely covered with mining concessions, either active or pending. According to Professor Christopher de Wet from Rhodes University in South Africa, who specialises in resettlements and rural development, the speed and scale with which the licences have been granted poses a challenge to the government in making sure that this is accompanied with the necessary measures to safeguard the affected populations:

“Resettlement is an incredibly complex thing – to pick people up and put them down somewhere else, you are not moving objects, you are moving a society,” says de Wet, raising concerns that the government of Mozambique may not be up to the task:

“You can have the best policies in the world but without the political capacity, structures or will in place to implement and enforce them, they are useless,” he says.

The farmer Delvino Xadreque, 37, was compensated with building materials for a barn, chickens and some feed by the Brazilian mining company Vale, when he, his four children, aunt and nephew were resettled, because the area they used to live in was expropriated for coal mining. But the chicken business has turned out with no profit. Before he had land, now he doesn't even though he was promised compensation for that as well. Photo: Jesper Kirkbak

Poor conditions in Mualadzi

About eight kilometres further up the winding road that cuts through Cateme lies another resettlement community, Mualadzi. Here, far from the main road that leads to the nearest town, people in Cateme are considered fortunate.

“They are lucky because they have transportation to town and a school for their children,” says Tito Fernando, a young father of three. Before the resettlement, he used to make bricks and sell them by the roadside, but the remote location of Mualadzi and an insufficient water supply makes it impossible for him to continue his trade. Instead, he and his wife take turns in travelling to Moatize town to sell some crops at the market. But it is a long journey with little outcome.

“She left this morning and I don’t know when she will be back, because she has to travel by three different cars to get here,” Fernando explains. He and his wife are among the 736 resettled families (approx. 3,680 people) in Mualadzi, struggling to make a living for themselves. Danwatchhas spoken to several members of the community and they tell similar stories about their efforts to get food on the table and make the scarce water resources cover their basic needs.

The resettlement was initiated by the Australian mining company, Riversdale, and British-Indian Tata Steel in 2010, when they started developing what would become the largest coal mine in Mozambique, covering 4,560 hectares in central Tete. Shortly after, the process was taken over by the British-Australian mining company, Rio Tinto, when the company bought Riversdale and held the majority ownership of the Benga mine in 2011. Soon after the takeover, Rio Tinto began the main phase of the resettlement process, moving 358 families from their villages in the mining area to Mualadzi.

The move meant a significant change for the families. They used to live in the villages Capanga and Benga Sede by the Revuboè and Zambezi rivers, near the main road leading to Tete city: this was a location with unrestricted access to water and to the fertile soil near

the river and near to town markets. The river not only provided the villages with water for people and their livestock but was also a place for leisure, where women could undress, wash their clothes and bathe freely, while their husbands, sons and fathers had their own section of the river to themselves.

Emilia Fato, a 58-year-old widow who lives with her son and two grandchildren, is longing to go back to her old life near the riverbank.

“Where we use to live, we had water from the river. There, we could provide for ourselves and we didn’t need help from anybody,” she says. She and her family used to grow crops, break stones and sell them for construction. In Mualadzi, they feel lost.

“My son was supposed to work, but he is just sitting here all day, because there is nothing for him to do. If we were home, I would know what advice to give him, but here I don’t

know what to tell him,” she says.

Before the resettlement to the Mualadzi area, Tito Fernando used to make bricks and sell them by the roadside, but the remote location of Mualadzi and an insufficient water supply makes it impossible for him to continue his trade. Instead, he and his wife takes turns in travelling to Moatize town to sell some crops at the market. But it is a long journey with little outcome. Photo: Jesper Kirkbak

No way out of Mualadzi

The Mualadzi resettlement site is 50 kilometres from the river and 40 kilometres from the closest town, Moatize. It is a place so remote it makes it almost impossible for the resettled to survive as a society, according to civil society organisations Oxfam, Human Rights Watch and SarWatch. Reports all point to food and water insecurity as a matter of great concern for the communities.

In the 2015 report Mining Resettlement and Lost Livelihoods, Australian Oxfam described Mualadzi as “a remote location with poor quality soil and an insecure supply of water for personal and agricultural use,” and stressed the gravity of the situation: “This harsh physical environment has put livelihoods at risk with food security being an immediate

challenge.”

The land that was given to the families who used to rely partly on subsistence farming is not suitable for crops and with half a day’s journey to the nearest town they struggle to find alternative ways to make a living. To Tito Fernando, the situation is desperate:

“It is very bad here, we have a lot of problems with both transportation and water. Sometimes we spend months without water,” he says, explaining that when water is in short supply, they resort to using the small creeks in the outskirts of the community. When asked about his thoughts about the future, his face hardens:

“Our future doesn’t look good. We see that. My children and I, we don’t have anything. There is an entrance to Mualadzi, but there is nowhere out. They just left us here.”

Compensation can impoverish

The food and water insecurity in Mualadzi and the remote location that offers little opportunity for the community to connect with other villages goes against both national law and international guidelines that say that resettlement cannot happen if it changes people’s living standards for the worse. Even though people in Mualadzi have been given material compensation, the new houses being of a far better quality than the wooden cottages they left behind, they are still struggling to get back on their feet after the move.

This comes as no surprise to Professor Christopher de Wet from Rhodes University in South Africa, who finds it meaningless to speak of compensation as a simple matter of one asset replacing the other.

“People in Mualadzi and Cateme have technically been compensated, but in fact they are worse off. They have been moved to land of lower quality and they are further from transport networks, which makes it difficult for them to market their goods. In that sense compensation can actually impoverish you,” he says. He stresses the complexity of

resettlements:

“Let’s say you have a trader. You can compensate him for the size of his shop and for his goods, but that most precious thing of all, those relationships of trust, which are actually what his livelihood depends on. How will you compensate him for that? That is what resettlement destroys, and these are the complex issues that compensation doesn’t

begin to touch.”

How to survive with limited access to water and food

7

Both the government of Mozambique and the mining companies Rio Tinto and Riversdale Mining Ltd. knew that the resettlement of 736 families to the remote area of Mualadzi would severely deteriorate their living conditions, long before they moved the communities.

This goes against Article 86 of Mozambique’s constitution and the national Mining Law, which state that people cannot be resettled if it changes their living standards for the worse, and international guidelines defined by the World Bank and enforced by the International Finance Corporation, IFC, stating that involuntary resettlement “should be conceived as an opportunity for improving the livelihoods of the affected people and undertaken accordingly.”

Danwatch has obtained the Benga Resettlement Action Plan (RAP) that guided the process of moving local communities away from the Benga mine concession area in Tete, Mozambique. It clearly describes Mualadzi as an area lacking sufficient water resources:

“The surface water resources are poorly developed in the area with no perennial water course running within or nearby the development area. The existing seasonal streams are highly dependent on the wet season for their flow pattern and therefore cannot be considered a continuous water source,” the RAP states.

Knowing the poor water conditions in the area, the mining company Riversdale Mining Ltd. and the Tete provincial government chose Mualadzi as the new home for the communities, and moved them to the remote site before further investigation into the water availability had been concluded and long before a solution was found, the RAP shows.

Moved according to schedule

In 2010 Riversdale Mining Ltd. began the resettlement process by moving people and livestock 43 kilometres away from their villages in order to make way for their Benga coal-mining project. Shortly after, Riversdale Mining was taken over by the third largest mining

company in the world, Anglo-Australian Rio Tinto, while British-Indian Tata Steel kept its 35 percent stake in the mine. Along with the majority ownership came the responsibility to finalise the resettlement of all affected communities.

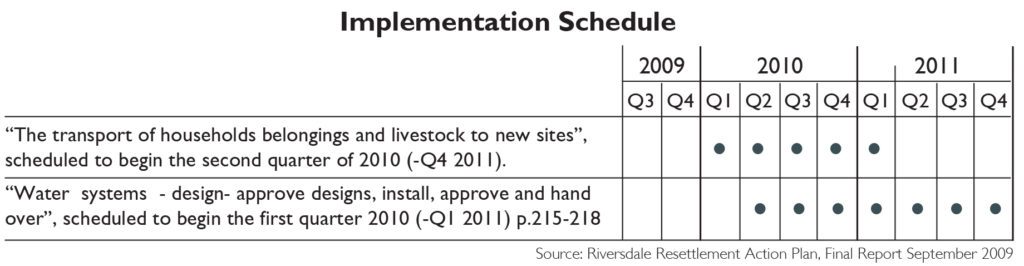

In 2011 Rio Tinto carried out the largest phase of the resettlement by moving 358 families to Mualadzi. Because water resources were poorly developed in the area, a technical team was to design and install water systems that could make up for the lack of natural water in the area. But according to the RAP from 2009, Riversdale and the government knowingly moved people to Mualadzi before a solution had been found.

The transportation of families and livestock was scheduled to take place while the technical team was still researching the water conditions in the area – and a year before a solution would be put in place – according to the implementation schedule included in the plan: The RAP further shows that if no sustainable solution to the water problem was found, the company and the government would need to find an alternative resettlement site.

“The water availability of the Mualadzi site will be confirmed during the implementation phase, but should this prove to be insufficient then a further process of site identification will be undertaken.”

Lack of food and water

When Rio Tinto took over the process of resettlement, the company continued along the lines set out by Riversdale Mining and moved more than 300 families to Mualadzi. To make up for the water shortage, Rio Tinto drove water tanks to the resettlement site where people could fill their water containers. But the water supply was unreliable and the community would sometimes wait in days for the next delivery, according to a report from Human Rights Watch, which conducted a large survey in the area in 2013.

Today, field research from Danwatch shows that people still deal with the aftereffect of the resettlement to Mualadzi. They have lost their livelihoods, and years of food and water scarcity has pushed the community to the verge of desperation. Several sources describe how water shortage poses an immediate challenge. One of them is 37-year-old Josefina Torres:

“We don’t have enough water, so we need to wash where the cows are drinking,” Torres says. For the mother of five, the question of how to get enough food and water for her children is a daily concern. She and her husband are trying hard to make ends meet in their new life:

“There is no work for us here. We used to make bricks and break stones for construction, but here we don’t know what to do. We are hungry, and sometimes we only have one meal per day,” she explains.

The family was given a small piece of land when they came to Mualadzi, but the lack of water makes it nearly impossible to grow anything in the soil, described in the RAP as “rocky” and “shallow,” so they currently live off a small store of maize from last year – far from enough to feed the family of seven, Torres says.

Josefina Torres, 37, and her family has been resettled to the Mualdazi area, because the area they used to live in was expropriated for coal mining. But the house they were given as compensation was too small. Her children, husband and a friend of the family have begun to make their own bricks to build an addition to the house. Photo: Jesper Kirkbak

Water loss was expected

The move to Mualadzi meant a drastic change for the affected communities that used to live in close proximity to the city, where unlimited access to the water running in the Zambezi and Revuboè rivers allowed them to cultivate their land all year round.

The Resettlement Action Plan shows that Riversdale Mining foresaw the challenges awaiting the families when they listed water availability as one of the anticipated losses connected to the move to Mualadzi. The plan describes how “the majority” of the affected families in Capanga rely on drinking water from the Revuboè river and other streams, especially during the dry season; it also describes how the families used to have access to community wells and how some had access to piped water outside their homes.

“These water sources will no longer be accessible to the affected households when they leave the EZ (exclusion zone, red.) and the Capanga area,” the plan states (p.116, list of key losses p.123). Paradoxically the choice of Mualadzi goes against Riversdale’s own criteria for host area selection, including “adequate and suitable existing or potential water supplies, occurrence of sufficient soils suitable for agriculture and easy access to the site.”

The criteria, however, are not prioritised and Riversdale make clear reservations,

stating that

“While the set of suggested criteria was applied (in the site selection, red.) it was recognised that: it would be unlikely that all the criteria would be met for any particular case. Thus, potential host areas which satisfied the greatest number of critical criteria were selected,” the plan reads.

RIVERSDALE’S CRITERIA FOR SITE SELECTION:

• Distance from Capanga

• Adequate and suitable existing or potential water supplies

• Occurrence of sufficient soils that are suitable for agriculture

• Occurrence of sufficient land that is suitable for livestock grazing

• Low potential for mining activities (i.e. no mining titles or low possibility of mineral deposits)

• Easy access (or low cost to provide access to the site)

• Presence of adequate social infrastructure (or low cost of providing new infrastructure)

• Presence and size of any host community living in the area

Source: The Resettlement Action Plan, September 2009, p.146

A question of rights

Despite the fact that mining-induced resettlements have been going on for years in Mozambique, no laws existed to regulate the resettlement processes itself until 2012 when the Resettlement Decree was issued, says Dr. Jose Macuane from the Eduardo Mondlane University in Maputo, who researches political economy and natural resources. But where specific legislation on resettlements falls short, other laws apply:

“This is essentially a rights issue. According to national law, companies should restore or improve the living conditions for the affected people, and the government should make sure that it happens, but the government in Mozambique hasn’t been effective in this,” he says.

According to the country’s Land Law legislation that defines the rights to land use and rules of compensation, individual citizens, communities or other entities who occupy land in good faith and according to customary practices have the right to unlimited use and benefit from that land, a right which may only be taken away by fair compensation. Still, the conditions in Mualadzi have not caused the companies or the government to find an alternative, more hospitable location for the families.

Communities are left in the dark

Before Mualadzi was chosen as the resettlement site, the communities in Capanga were wary about the location. They questioned whether the soil was suited for agriculture and they were concerned about the distance to Tete and the Moatize markets, the Resettlement Action Plan shows.

According to the plan, the community’s concerns about the resettlement site were put forward on at least three different occasions. At a general meeting in February 2009 the community expressed concern about the location and conditions present in Mualadzi. In July 2009 they stressed the need for a location with sufficient water resources that would allow them to produce crops all year round, like they were used to. Similar points were made during focus group discussions in the same period.

THE RESETTLEMENT ACTION PLAN SHOWS:

1. The companies knew about the difficult water conditions.

2. Implementation of the Resettlement Action Plan, including the first transport of people to Mualadzi, was scheduled to commence before a solution had been found to the water issue.

3. Riversdale and the government would need to find an alternative resettlement site if no sustainable solution to the water problem was found.

4. Reduced water availability figures on the list of anticipated losses connected to the move to Mualadzi.

The plan summarises the conditions put forward by the communities, which contains demands like a location near a riverbank, good soils for fields (machambas) and grazing, access to Zambezi and Revuboè islands and houses and other structures – structures such as cattle pens and chicken coops must remain close to the main residential structure for better control of the livestock.

Contrary to the community’s wishes and despite the questionable conditions in the area, the government and Riversdale selected Mualadzi as a suitable resettlement site, while acknowledging the “lack of consensus.” To date, a permanent solution to the water issue has not been found, and the community in Mualadzi still relies on the current owners of the Benga mine, ICVL and Tata Steel, for their water supply.

Mining company: Too soon to judge

Danwatch has contacted all the implicated mining companies and presented them with our findings. Rio Tinto, which moved the largest group of people to Mualadzi, has declined to say why the company did not put an alternative plan into play when faced with the realities in Mualadzi.

The right to an adequate standard of living, including the right to water, is protected by article 11 in the UN International Covenant of Economic, Social and Cultural Rights (ICESCR). In a business setting, it means that companies should take “reasonable steps to ensure that their operations do not adversely impact the availability, accessibility and quality of clean water, both in the short and long term,” according to the consultancy

Global CSR in a guidebook to business.

Rio Tinto, known for its strong CSR profile, also subscribes to the standards outlined in the IFC Handbook on Preparing a Resettlement Action Plan, which serves as the only comprehensive corporate guide dealing explicitly with the complex issue of involuntary resettlement. In a written statement to Danwatch from 13 August 2015, Rio Tinto

states:

“We take our responsibilities to local communities seriously and to the point of transfer, our activities worked to meet internal and international standards. This is difficult and complex work and its success cannot be judged after 12 months, two or even five years. In particular, livelihood restoration for households takes time given the multi-year nature of this process.”

The Right to Resettle

Danwatch have asked Rio Tinto how the company’s standards comply with its involvement in the resettlement of hundreds of families, but they have declined to answer the question. The responsibility lies with the government and the current owner ICVL, they say, stressing that “the Government of Mozambique reserves the right to choose and provide the land on which to resettle populations and this was the case with the Benga Mine

resettlement.”

According to Tata steel, who holds 35 percent of the shares in the Benga mine, the company “has no executive part in leadership decisions regarding the Benga mine.”

IFC (INTERNATIONAL FINANCE CORPORATION) PRINCIPLES FOR INVOLUNTARY RESETTLEMENT

Involuntary resettlement should be avoided. Where involuntary resettlement is unavoidable, all people affected by it should be compensated fully and fairly for lost assets.

Involuntary resettlement should be conceived as an opportunity for improving the livelihoods of the affected people and undertaken accordingly. All people affected by involuntary resettlement should be consulted and involved in resettlement planning to ensure that the mitigation of adverse effects and the benefits of resettlement are appropriate and sustainable.

Source: IFC Handbook on Preparing a Resettlement Action Plan

Danwatch has asked Tata Steel if it has taken or plans to take any steps to actively improve the situation in Mualadzi, but the company has not given an answer.

ICVL has been presented with the findings of this investigation but has not responded.

Before Mualadzi was chosen as the new home for the displaced families, community members continuously stressed that year-round water availability was a key conditions for the resettlement site. Worried about the remote location of Mualadzi, they preferred another site closer to their homes in Capanga and Benga Sede near the Revuboè and Zambezi rivers, the Resettlement Action Plan shows.

The plan offers no explanation why Mualadzi was chosen as the most suitable location, other than the fact that it was free of mining concessions.

LAND LAW NO. 19/97:

According to the Mozambican Land Law that defines the rights to land use and rules of compensation, individual citizens, communities or other entities

who occupy land in good faith and according to customary practices have the right to unlimited use and benefit from that land, a right which

may only be taken away in exchange for fair compensation.

THE NEW CONSTITUTION OF MOZAMBIQUE (1990):

The right to compensation is also secured in article 86 of the new constitution of Mozambique, which states that individuals and other entities have

the right to “equitable compensation” for expropriated assets and the right to a new and equal plot of land.

THE RESETTLEMENT DECREE:

The Resettlement Decree of 2012 defines the basic rules and principles of the resettlement process “with a view to the promotion of the citizens’

quality of life and the protection of the environment.” (Note: The decree was issued after the Resettlement Action Plan for the Benga Mine was

prepared.) Available at: http://www.acismoz.com

Q & A on Coal & Steel

8

What is coking coal?

Coking coal is a vital ingredient in steel production all over the world. Coking coal, also known as metallurgical coal, is used to make coke, one of the key irreplaceable inputs for the traditional production of steel.

Who are the 10 largest exporting countries of coking coal?

Australia, USA, Canada, Russia, Mongolia, Mozambique, Indonesia, Poland,

Czech Republic, New Zealand

So why is Mozambique interesting?

In 2013 Mozambique was among the top ten coking coal exporters with 4 million tons, putting the country in sixth place, according to the World Steel Association. Despite a drop in global coal prices, which has caused companies and investors to hold their breath, KPMG International projects that Mozambique’s mining sector is on track to become one of the largest coal exporters globally by 2017.

The Tete province in Mozambique holds an estimated 23 billion tons of mostly untapped coal reserves. According to estimates from Environmental Justice Atlas, only 60 percent of the province’s area is used by the extractive industry, which accounts for around six million acres of land. Mozambique is also “set to benefit from large coal demand from China and India and could well become one of the 10 largest coal exporters globally

by 2017,” according to KPMG.

According to African Economic Outlook, Mozambique’s economy continued to perform strongly in 2014 with GDP growth of 7.6 percent and the outlook remains positive. Sustained growth is expected at 7.5 percent in 2015 and 8.1 percent in 2016. As in previous years, the main drivers of growth will continue to be public expenditure and FDI.

Who were the first moving mining companies in Mozambique?

According to US Geological Survey:

In November 2007, ArcelorMittal acquired a 35 percent interest in Black Gold Mining (Moc). In December 2007, Riversdale Mining Ltd. of Australia announced the signing of a joint-venture agreement with Tata Steel Ltd. of India to develop a mine in the Moatize coalfield. Tata purchased a 35 percent share in the Benga and the Tete licences that were held by Riverside.

The Brazilian mining company Vale estimated a production of 12 million tons of coking and thermal coal a year starting from 2010 at the Moatize Mine. The life of the Moatize Mine was expected to be 35 years. In 2007, Central African Mining and Exploration Company (CAMEC) of the United Kingdom engaged in drilling in. CAMEC also went into a joint venture for three licences in the Zambezi Coal Basin in Tete Province. In 2010, Camec was bought Eurasian Natural Resources Corp.

What’s the capacity of the mines in Mozambique today?

Vale is the majority shareholder (81 percent) of the Moatize mine. Vale projects coal production at the Moatize mine to reach 11 million tons a year by mid-2016, rising to 22 million tons a year in 2017, according to African Transparency initiative Asoko Insight.

The Benga mine is one of the largest mines in Africa, covering an area of more than 4,000 hectares. The Benga mine has the capacity to produce 5.3 million tons of coal per year, currently producing 4 million tons. The owner of the Benga mine, ICVL, is planning to expand its capacity to 13 million tons in five years. Tata Steel owns 35 percent of the Benga mine.

How much of the coking coal is going to Europe?

There are no exact numbers for how much of the Mozambican coking coal is exported to Europe. Around 1.2 billion tons of coal are used in global steel production, which is around 15 percent of total coal consumption worldwide, according to World Coal Association. This investigation shows that the largest crude steel producers in the EU rely on coking coal from Mozambique.

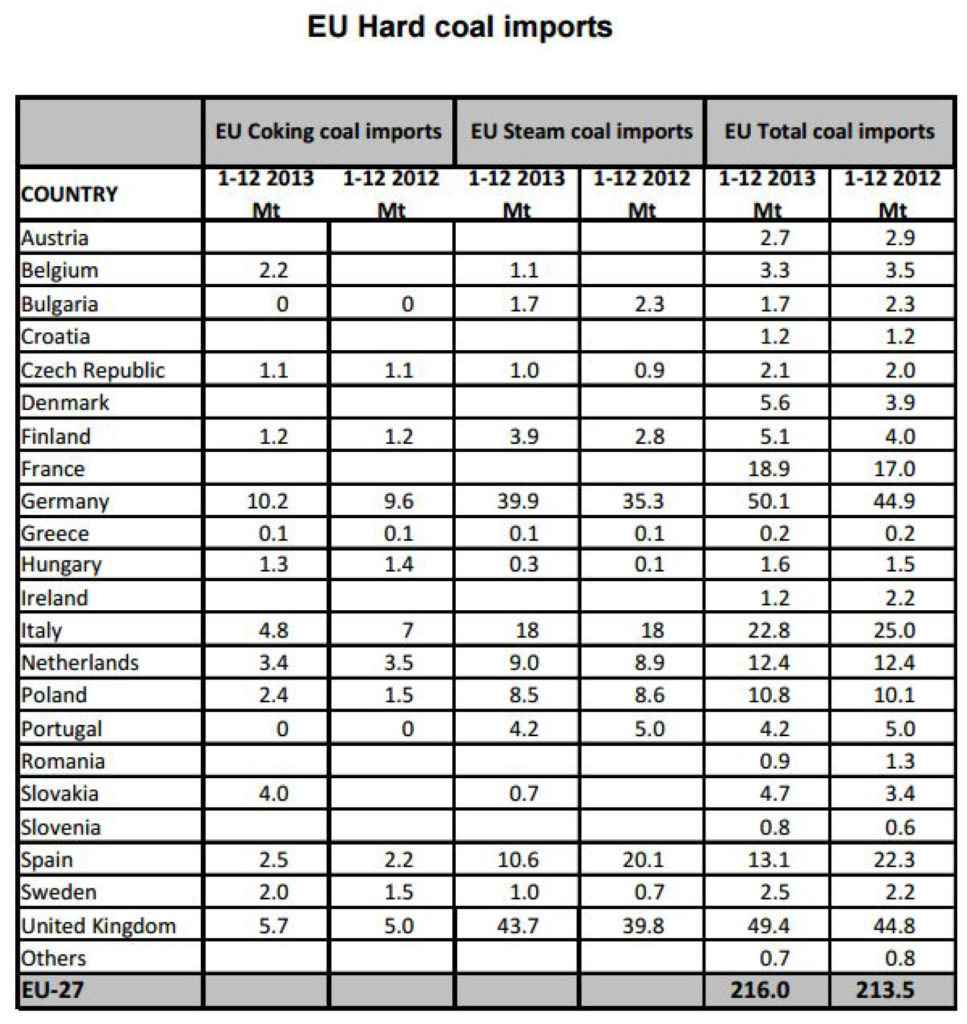

70 percent of total global steel production is dependent on coal. EU imported 40,9 million tons coking coal in 2013, an increase since 2012 where EU imported 34,1 million tons, according to Eurocoal.

Who are the top 10 coal importing countries?

China, Japan, India, Korea, Ukraine, Brazil, Germany, Chinese Taipei, United Kingdom, Turkey.

Source: World Coal Association

How EU steel production is violating human rights

9

The largest steel producers in Europe source coking coal from Mozambique where mining companies have displaced thousands of people in order to make way for their large-scale projects. The investigation ‘Broken Promises’ documents how international mining corporations knowingly, and with the approval of the government of Mozambique, have resettled local communities to remote areas with limited access to jobs, food and water. When asked about their supply chain most steel companies claim confidentiality.

Strategically placed on the South Eastern coastline of Africa with ports opening the country to the sea lanes of the Indian Ocean, and with an underground full of largely untapped coal resources, Mozambique is today the world’s fifth largest exporter of coking coal, with approximately 4 million tonnes leaving the Port of Beira every year, some of it headed to feed a growing European market. According to Euracoal, the European demand for coal is increasing, mainly lead by Germany and the UK, and in 2013 European countries imported a total of 40,9 million tons of coking coal.

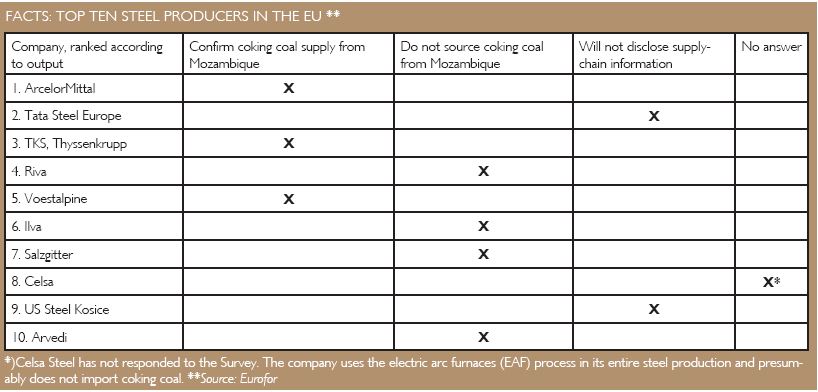

Results from a Danwatch survey sent to the ten largest steel producers in Europe, combined with research into company documents, show that ArcelorMittal, Tata Steel Europe, TKS ThyssenKrupp, and Voestalpine source coking coal from Mozambique. Danwatch has asked all ten companies to disclose their suppliers and to identify which mines they source from.

No interviews about suppliers or partners

According to national news agency Bloomberg, Tata Steel is entitled to 40 percent of the outcome from the Benga mine. On the 18th of May 2012 the company’s main director H.M. Nerurkar announced that Tata Steel Europe would receive its first supplies from the mine that month – approximately 800.000 tons, equivalent to 10 percent of is entire coal

requirements, Bloomberg reported on May 22nd 2012.

The Slovaki steel company U. S. Steel Košice, ranking as number 9 on the Eurofer top ten list, has declined to answer the survey.

“I can confirm that we do not provide information about our business partners, suppliers or customers and that we do not want to participate in the survey,” Ján Baĉa, the company’s spokesperson writes in an e-mail to Danwatch. He has since declined to participate in an interview.

Companies claim supply chain oversight

The internationally recognized guidelines for corporate responsibility, the OECD Guidelines for Multinational Enterprises and the UN Guiding Principles for Businesses and Human Rights, set clear standards for responsible supply chains.

According to OECD, companies should practice due diligence by investigating third party partners for potential abuse of human rights; set forward standards for corporate behaviour and: “Seek ways to prevent or mitigate adverse human rights impacts that are directly linked to their business operations, products or services by a business relationship, even if they do not contribute to those impacts.”

This investigation shows that the largest steel producers in Europe source coking coal from Mozambique, where mining companies have displaced thousands of people, and in the cases of Mualadzi and Cateme, deprived communities of their livelihoods and limited their access to food and water.

COMPANIES CLAIM CONFIDENTIALITY

Voestalpine and Tata Steel Europe inform Danwatch that they source coking coal from Mozambique, but they do not wish to disclose the size of their import or from which mines. Voestalpine has declined to answer any further questions, and Tata Steel Europe has declined to answer whether it sources from the Benga mine, of which its parent, Indian Tata Steel, owns 35 percent.

Three of the top-ten steel producers in this investigation can be linked directly to these resettlements through their supply chain.

ArcelorMittal, Tata Steel Europe and ThyssenKrupp have declined to answer any questions directly related to the situation in Cateme and Mualadzi. But in their general statements to Danwatch they refer to both international guidelines and company policies, stressing responsible sourcing and supply chain oversight as a common priority.

The responsibility to respect human rights

The UN Guiding Principles for business and Human Rights establish that while states have the responsibility to protect human rights, companies have the responsibility to respect them. To meet that responsibility companies should have

“(a) A policy commitment to meet their responsibility to respect human rights; (b) A human rights due diligence process to identify, prevent, mitigate and account for how they address their impacts on human rights; c) Processes to enable the remediation of any adverse human rights impacts they cause or to which they contribute.”

Neither Tata Steel Europe, Voestalpine nor ArcelorMittal refer to international guidelines in their answers to Danwatch, ThyssenKrupp however states, that the company expects all its suppliers to comply with with the principles of the United Nations Global Compact, and that the company carries out sustainability audits at individual suppliers.

“The suppliers are selected on the basis of a systematic assessment of risks, in particular country-related risks. This also includes our raw material suppliers.”

Since Danwatch received the statement from Thyssenkrupp, the company has been presented with the findings in this investigation. Thyssenkrupp has declined to comment on the conditions in Cateme and Mualadzi and refer to their general statement, where the final paragraph reads:

“Should a supplier demonstrably fail to meet the standards of the ThyssenKrupp Supplier Code of Conduct or fail to target and implement improvement measures, this can ultimately lead to termination of the business relationship.”

All company statements can be found in full, in Annex 1.

FACTS: THE CHIPANGA MINE

The Chipanga mine, located in the Province of Tete is owned by Brazilian miner Vale. It has a total capacity of 11 million metric tons per year, Only one company, German ThyssenKrupp has informed Danwatch about its supply chain, listing Vale’s Chipanga mine and Rio Tinto’s Benga mine (now ICVL, red.) as their suppliers in Mozambique. However, company reports from the largest steel producer in Europe, ArcelorMittal,

confirm that the multinational company started sourcing from the same mines by 2012.

“In 2012 and 2013, ArcelorMittal further diversified its supply portfolio by adding new supply sources from emerging mines in Mozambique and Russia,” a paragraph reads in the 2013 Annual Report for the United States Securities and Exchange Commision, and in the company’s 2014 Annual Report, Vale and Rio Tinto in Mozambique are listed as

some of ArcelorMittal’s “principal coal suppliers” .

Source: ThyssenKrupp

FACTS: THE BENGA MINE

The mine is located in the Tete province of Mozambique, and is part of the Benga Coal Project, initially owned by Tata Steel and Australian concern Riversdale Mining. In November 2007, Tata Steel purchased a 35 percent stake in the project. In April 2011, British-Australian Mining Company, Rio Tinto, took over Riversdale Mining Limited, and its 65 percent share in the Benga Coal Project. In 2014, Rio Tinto sold its shares to the Indian steel and mining company ICVL. Around 35 percent of the mine’s output is coking coal, 10 percent thermal coal, and the remaining 55 percent is waste. From 2010-2014, Riversdale Mining Limited, Rio Tinto and Tata Steel moved 736 families to the Mualadzi

resettlement.

Source: www.tatasteel.com

Behind The investigation

10

‘Broken Promises’ is a journalistic investigation based on desk research and expert interviews conducted in May 2015, and on field research in Tete province and Maputo, Mozambique, in June 2015. During field research, Danwatch interviewed several community members from the resettlements in Mualadzi and Cateme who blame mining companies and the government of Mozambique for not living up to the commitments they made in the community resettlement process from 2010 until the present. A documentary, ‘Promised Land’, was produced based on the findings from Mozambique in this report.